When you transition into the fast-paced world of day trading, your focus naturally lands on mastering technical chart patterns and optimizing entry signals. It is incredibly easy to overlook the silent operational friction that strips away your capital efficiency before a trade even has room to breathe. Sourcing an optimized fee structure is not just a secondary administrative preference; it is a core math requirement that alters your long-term probability of survival.

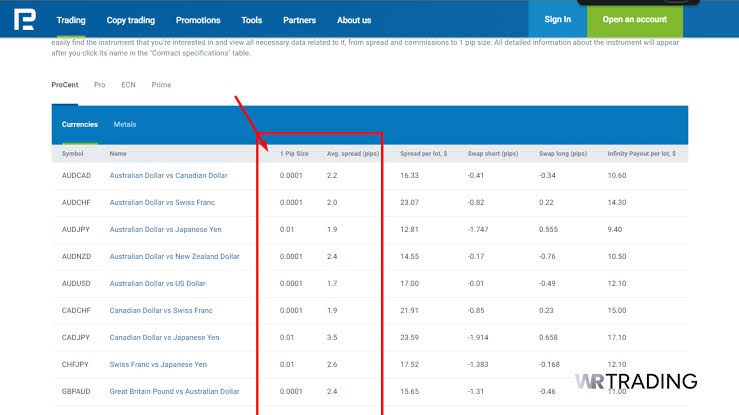

Analyzing contract specifications and variable spread metrics on a platform layout. Source: WR Trading

What exactly is the difference between a standard spread and a raw spread?

The divide comes down to how your platform routes and marks up price data before it reaches your terminal layout. On a standard account, the broker takes the genuine wholesale quotes streamed by interbank liquidity pools and adds an artificial markup layer to build an internal profit margin.

A raw spread layout strips this retail padding away completely. Your terminal connects directly to raw wholesale interbank feeds where major global banks compete to match your orders. Think of this setup like buying your merchandise straight from a commercial warehouse floor instead of a retail storefront. The visual gap between your buying and selling prices collapses to bare minimum fractions, allowing you to access the market at its truest structural boundary.

Why does a fractional difference in pips matter so much to a day trader?

For multi-day swing traders targeting massive hundred-pip moves, a minor pip fraction functions as background white noise. The math turns completely upside down when you operate on an intraday day trading or short-term scalping model.

Day traders survive by capturing quick, bite-sized price runs throughout a single session. The bid-ask spread behaves exactly like a non-negotiable entry toll or service charge paid upon execution. If your average take-profit target is ten pips, a padded standard spread of 1.5 pips means you are volunteering to hand over 15% of your gross profit potential the exact millisecond your order fills. Reducing that toll to a raw 0.1-pip average protects your mathematical edge, keeping the vast majority of that yield inside your account balance.

If the raw spread is near zero pips, how does the broker make a profit?

No enterprise functions as a charity, so when a platform removes the retail markup from your charting panel, they unbundle their fee structure entirely. They replace the floating, hidden padding by charging a transparent, flat ticket commission fee per standard lot traded instead.

This configuration gives you absolute cost visibility. You exchange the slippery uncertainty of a wider floating gap for a predictable, fixed administrative fee that stays locked regardless of minor market ripples. Utilizing a professional environment backed by modern low spread forex brokers ensures you secure this unbundled efficiency. Your accounting stays remarkably clean because your positions break even almost immediately upon execution, rather than forcing the chart to make a massive directional jump just to clear a retail markup wall.

How do raw spreads alter my technical risk-to-reward parameters?

Standard account markups act like a heavy weight tied to your strategy’s compounding engine, quietly expanding your downside exposure while cutting your realistic upside potential. Symmetrical friction alters your execution parameters behind your back.

Suppose you set up an intraday position targeting a clean 15-pip profit with a tight 10-pip stop-loss boundary. If you execute that ticket inside a 1.5-pip standard spread environment, your realistic reward shrinks to 13.5 pips while your real downside risk stretches out to 11.5 pips. Your pristine 1:1.5 risk-to-reward ratio has instantly degraded into a far less competitive 1:1.17 model. Over a massive sample size of hundreds of sequential entries, this mathematical decay forces you to maintain an unsustainably high win rate just to keep your portfolio afloat.

Can choosing better platform software enhance this raw fee framework?

All the institutional pricing depth in the world means very little if your localized terminal infrastructure suffers from data bottlenecks. A slow, unoptimized platform application will lag behind the live interbank matching engines, filling your commands at inferior tiers during sudden volatility drops.

Sourcing an enterprise-grade workspace, such as the best forex broker for mt5, ensures your software can process high-speed multi-bank data streams simultaneously. Advanced execution suites feature ultra-low latency bridges that route your buy and sell parameters straight to global data hubs in milliseconds. This technical compatibility allows you to deploy high-frequency automated scripts and indicators that capture tight wholesale prices before the order ledger can slip away.

What practical adjustments should I make to maximize my raw spread efficiency?

Trading on raw pricing requires adjusting your execution timing to align with global volume peaks. Even the most advanced ECN infrastructure cannot maintain razor-thin spreads when global banks close their desks for the evening.

Avoid forcing market entries during the low-volume dead zone right after the New York financial session wraps up for the day. Restrict your active trading hours strictly to major session overlaps, such as the high-volume window when London and New York clearings run concurrently. Deep liquidity guarantees maximum matching competition among prime bank desks, locking your raw fees down to absolute historical floors and ensuring your day trading framework operates at its maximum mathematical capacity.

Practical Takeaway

Stop treating transaction fees as an abstract detail on your workspace, and start tracking them as a primary operational expense. Pull your statement logs from the past thirty days, calculate your aggregate lot volume, and run the math to see exactly how much capital is sliding through your platform’s pricing setup. By migrating your active portfolio away from padded retail accounts and focusing your execution exclusively inside peak liquidity windows using limit orders, you can eliminate structural fee leaks and run your day trading with absolute mathematical discipline.